4 Economic Concepts Every Consumer Should Grasp

In our daily lives, whether we realize it or not, we're constantly navigating the currents of economics. From deciding what to buy at the grocery store to contemplating a major investment, economic principles shape our choices. Understanding these principles not only empowers us as consumers but also sheds light on the intricate workings of the world around us. Here are four fundamental economic concepts that every consumer should be acquainted with:

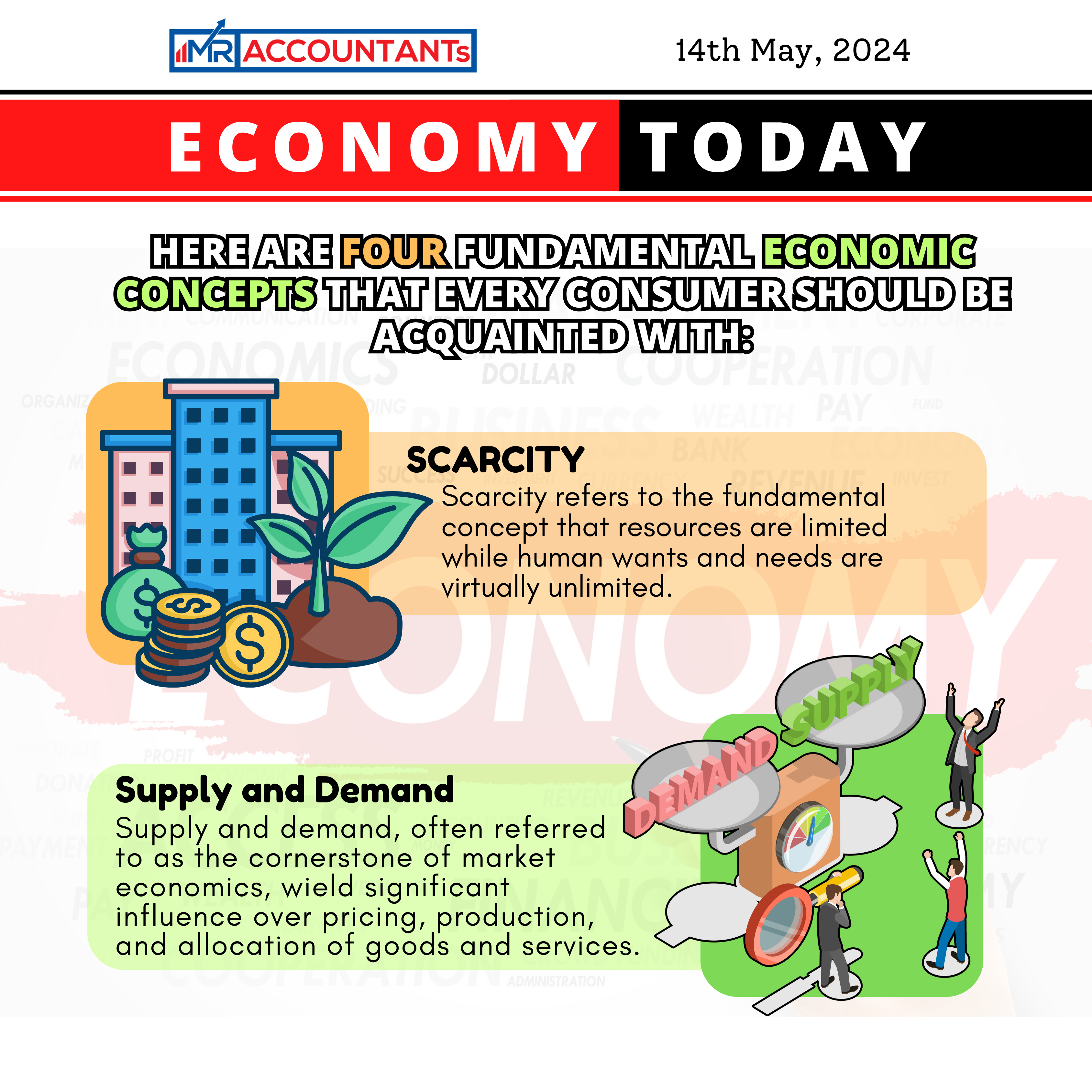

Scarcity:

At its core, scarcity encapsulates the fundamental imbalance between the limited availability of resources and the unlimited desires of individuals. This disparity is inherent in virtually every aspect of our lives, from the most mundane daily choices to the most significant global challenges. Whether we're considering personal finances, environmental sustainability, or national economic policies, scarcity is a pervasive and influential force shaping our decisions and outcomes.

Consider personal finances, for instance. Most individuals have a finite amount of money to allocate towards various expenses such as housing, food, transportation, entertainment, and savings. When making purchasing decisions, they must weigh the trade-offs between different goods and services. For example, spending money on a luxury item may mean sacrificing savings for future goals like retirement or education. This opportunity cost—the value of the next best alternative forgone—is a direct consequence of scarcity.

Moreover, scarcity extends beyond monetary resources to encompass time, energy, and natural resources. Time, perhaps the most precious resource of all, is limited and irreplaceable. Each day presents a finite number of hours, and how we choose to allocate our time reflects our priorities and values. Every hour spent on one activity is an hour not available for another—whether it's pursuing a hobby, spending time with loved ones, or advancing in our careers.

Similarly, natural resources like clean air, fresh water, and fertile land are finite and subject to depletion or degradation. The concept of scarcity becomes particularly salient in environmental contexts, where the overexploitation of resources can lead to ecological damage and threaten the well-being of present and future generations. Climate change, deforestation, and water scarcity are stark reminders of the consequences of mismanaging finite resources in the face of infinite demands.

Understanding scarcity is essential for consumers because it illuminates the necessity of making choices and trade-offs. By recognizing that resources are limited, consumers can adopt a more strategic and mindful approach to resource allocation. This may involve setting priorities, budgeting effectively, minimizing waste, and seeking alternatives that offer greater value or efficiency.

An awareness of scarcity can foster a sense of responsibility and stewardship towards resources, encouraging individuals to consume more responsibly and advocate for sustainable practices. Whether it's reducing personal consumption, supporting environmentally conscious businesses, or advocating for policy changes, consumers play a pivotal role in shaping the collective response to scarcity and its associated challenges.

Supply and Demand:

Supply and demand, often referred to as the cornerstone of market economics, wield significant influence over pricing, production, and allocation of goods and services. Let's unpack this concept further.

The Law of Demand and Supply:

The law of demand states that when the price of a good or service rises, the quantity demanded by consumers tends to decrease, and conversely, when the price falls, the quantity demanded tends to increase. This inverse relationship between price and quantity demanded is rooted in basic human behavior: as the cost of acquiring a good or service increases, consumers typically seek alternatives or reduce their consumption to maintain their utility or satisfaction.

Conversely, the law of supply posits that as the price of a good or service rises, the quantity supplied by producers tends to increase, and when the price falls, the quantity supplied tends to decrease. This positive relationship between price and quantity supplied reflects the profit motive of producers: higher prices incentivize increased production, as firms aim to maximize their revenue and profitability.

Equilibrium and Market Clearing:

The interaction of supply and demand culminates in the equilibrium price and quantity, where the quantity demanded equals the quantity supplied. This state of equilibrium, often depicted graphically as the intersection of supply and demand curves, signifies a balance between consumer preferences and producer capabilities. At this equilibrium price, there is no surplus or shortage in the market—supply matches demand, and transactions occur smoothly.

When supply and demand are in equilibrium, the market clears, meaning that all goods and services offered for sale are sold at the prevailing price. However, disruptions in supply or demand—such as changes in production costs, consumer preferences, or external shocks—can lead to shifts in the equilibrium, resulting in changes in prices and quantities exchanged.

Implications for Consumers:

Understanding supply and demand dynamics empowers consumers to anticipate changes in prices and make informed decisions about their purchasing behavior. For example, if consumers anticipate an increase in the price of a particular good due to high demand or limited supply, they may choose to buy it in advance to avoid higher costs in the future. Conversely, if consumers expect a decrease in price due to excess supply or decreased demand, they may postpone purchases to capitalize on lower prices later.

Moreover, consumers can leverage their understanding of supply and demand to assess the relative value of goods and services in the market. By comparing prices across different sellers and evaluating the responsiveness of quantity supplied and demanded to price changes, consumers can identify opportunities for cost savings and optimal allocation of their resources.

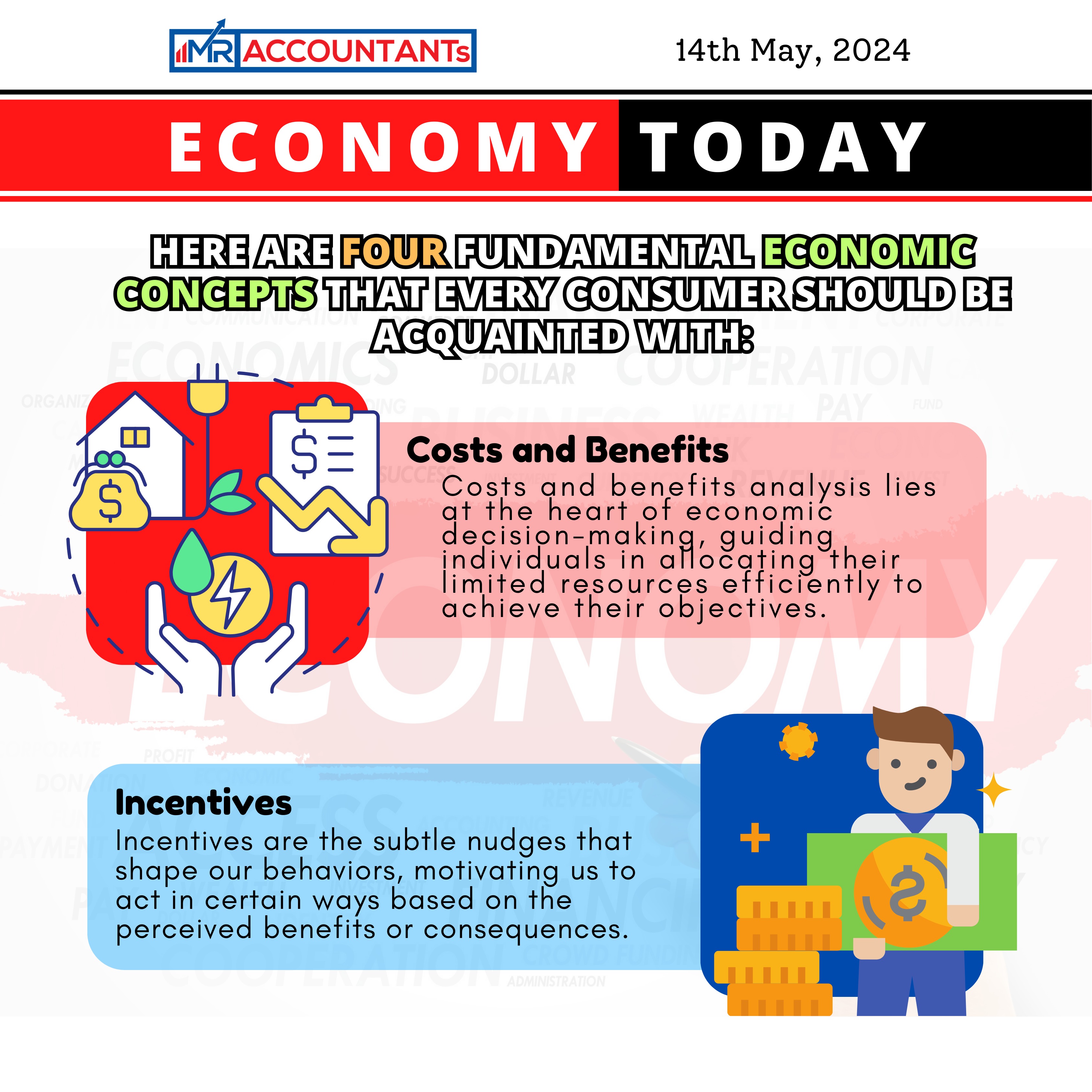

3. Costs and Benefits:

Costs and benefits analysis lies at the heart of economic decision-making, guiding individuals in allocating their limited resources efficiently to achieve their objectives. Let's explore this concept further.

Every decision we make involves a trade-off—a sacrifice of one thing to gain another. Costs represent what we give up to obtain something, whether it's money spent, time invested, or effort exerted. On the other hand, benefits encompass the value or satisfaction derived from a decision or action. Rational decision-makers seek to maximize their utility by selecting options that offer the greatest benefit relative to the cost incurred.

Monetary and Non-Monetary Considerations:

While monetary costs and benefits are readily quantifiable—such as the price of a product or the salary earned from work—non-monetary factors also play a crucial role in decision-making. Time, for instance, is a valuable resource with its own opportunity cost—the value of the next best alternative foregone by choosing one activity over another. Similarly, decisions may involve intangible benefits like emotional well-being, social status, or personal fulfillment, which are not easily quantified but nonetheless influence choices.

Opportunity Cost:

At the heart of costs and benefits analysis lies the concept of opportunity cost—the value of the next best alternative forgone when a decision is made. Every choice entails foregoing alternative options, each with its own set of costs and benefits. For example, choosing to attend a concert may mean sacrificing the opportunity to spend time with family or engage in a different leisure activity. By considering opportunity costs, individuals can evaluate the full spectrum of alternatives and make more informed decisions about how to allocate their resources effectively.

Aligning Preferences and Goals:

Ultimately, the goal of costs and benefits analysis is to align individual preferences and goals with the choices made. Different individuals may prioritize different factors—such as leisure, income, or personal development—based on their unique circumstances, values, and objectives. By carefully weighing the costs and benefits of various options, consumers can tailor their decisions to optimize their utility and achieve their desired outcomes.

Implications for Consumers:

For consumers, understanding costs and benefits is instrumental in making informed decisions about purchases, investments, and lifestyle choices. By comparing the costs and benefits of different alternatives, individuals can identify opportunities for maximizing value and minimizing waste. Moreover, considering the long-term consequences and opportunity costs of decisions can help consumers prioritize their goals and allocate their resources strategically over time.

4. Incentives:

Incentives are the subtle nudges that shape our behaviors, motivating us to act in certain ways based on the perceived benefits or consequences. Incentives serve as the driving force behind much of human behavior, influencing our decisions and actions in countless situations. Whether they're positive rewards for desirable behaviors or negative consequences for undesirable actions, incentives play a pivotal role in shaping our choices. From financial incentives like bonuses and discounts to social incentives like praise and recognition, the allure of rewards or the fear of penalties can significantly impact our decision-making process.

Rational Response to Incentives:

Economists often assert that people respond to incentives—that is, individuals adjust their behavior in response to changes in the incentives they face. This principle underscores the rationality of human decision-making, as individuals seek to maximize their utility or satisfaction by aligning their actions with the incentives at hand. For example, the promise of a cashback reward may incentivize consumers to use a particular credit card for their purchases, while the threat of a fine may deter motorists from speeding on the highway.

Anticipating Behavior:

Understanding incentives enables consumers to anticipate how others, such as businesses or policymakers, might behave in different situations. By analyzing the incentives faced by various stakeholders, consumers can make more informed predictions about their actions and adjust their own behavior accordingly. For instance, knowledge of a retailer's pricing strategy—such as offering discounts during off-peak hours—might prompt consumers to time their shopping trips strategically to capitalize on the savings.

Influence on Decision-Making:

Incentives permeate all aspects of economic decision-making, from consumer choices to business strategies to government policies. Businesses, for example, may use pricing incentives, loyalty programs, and advertising campaigns to attract customers and drive sales. Similarly, policymakers may employ tax incentives, subsidies, and regulations to promote specific behaviors or achieve societal goals. By recognizing the underlying incentives driving these actions, consumers can better understand the motivations behind them and make more informed decisions in response.

Empowering Consumers:

Ultimately, understanding incentives empowers consumers to navigate the economic landscape more effectively, making choices that align with their preferences and goals. By evaluating the incentives at play and considering their own priorities, individuals can make strategic decisions to maximize their utility and well-being. Moreover, a nuanced understanding of incentives can foster a more critical and discerning approach to evaluating the actions and policies of businesses and policymakers, enabling consumers to advocate for their interests and hold decision-makers accountable.

In conclusion, these four economic concepts—scarcity, supply and demand, costs and benefits, and incentives—serve as foundational pillars for understanding the choices we make as consumers. By grasping these principles, individuals can navigate the complexities of the market more effectively, make informed decisions, and ultimately improve their economic well-being. Whether you're shopping for groceries or contemplating a major purchase, a solid understanding of economics can help you make the most of your resources and achieve your goals.