Adjustments and Reclasses in Accounting

In the intricate world of accounting, accuracy is paramount. This requires meticulous attention to detail and the ability to make necessary corrections. Two fundamental processes to ensure this accuracy are adjustments and reclasses. This blog will explore these concepts, their importance, and how they contribute to the integrity of financial statements.

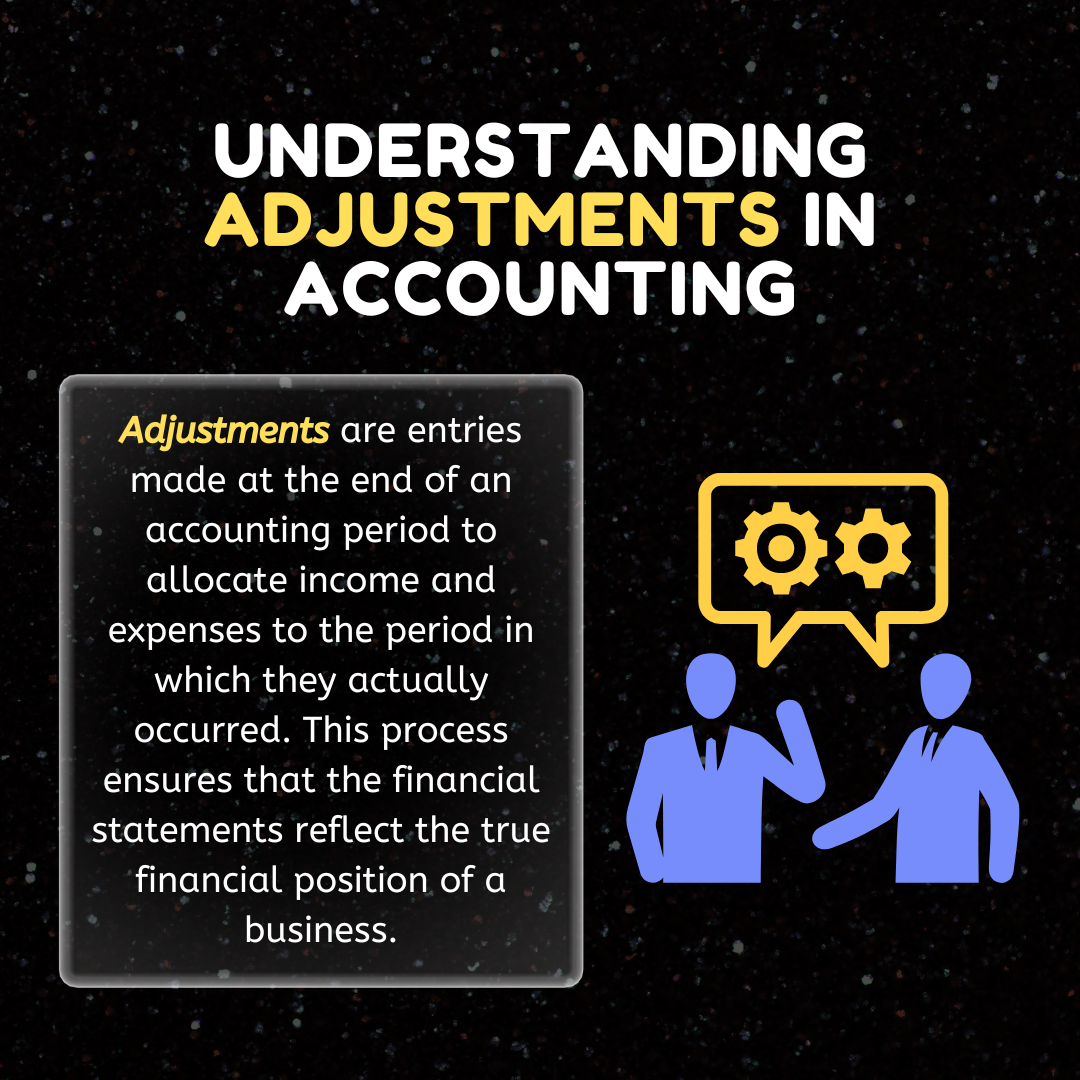

Understanding Adjustments in Accounting

Adjustments are entries made at the end of an accounting period to allocate income and expenses to the period in which they actually occurred. This process ensures that the financial statements reflect the true financial position of a business.

Types of Adjustments:

Accrued Revenues and Expenses:

Accrued Revenues: Revenues that have been earned but not yet recorded.

Accrued Expenses: Expenses that have been incurred but not yet recorded.

Deferred Revenues and Expenses:

Deferred Revenues: Revenues received in advance for services or goods to be delivered in the future.

Deferred Expenses: Payments made in advance for expenses that will benefit future periods.

Depreciation and Amortization:

Allocating the cost of tangible and intangible assets over their useful lives.

Inventory Adjustments:

Ensuring that the inventory records match the actual physical count.

Importance of Adjustments:

Accurate Financial Reporting: Adjustments ensure that revenues and expenses are recorded in the correct accounting period, providing a true picture of the financial health of the organization.

Compliance: Adjustments help in adhering to accounting standards and principles such as the matching principle and accrual basis of accounting.

Decision-Making: Accurate financial statements are crucial for stakeholders, including management, investors, and creditors, to make informed decisions.

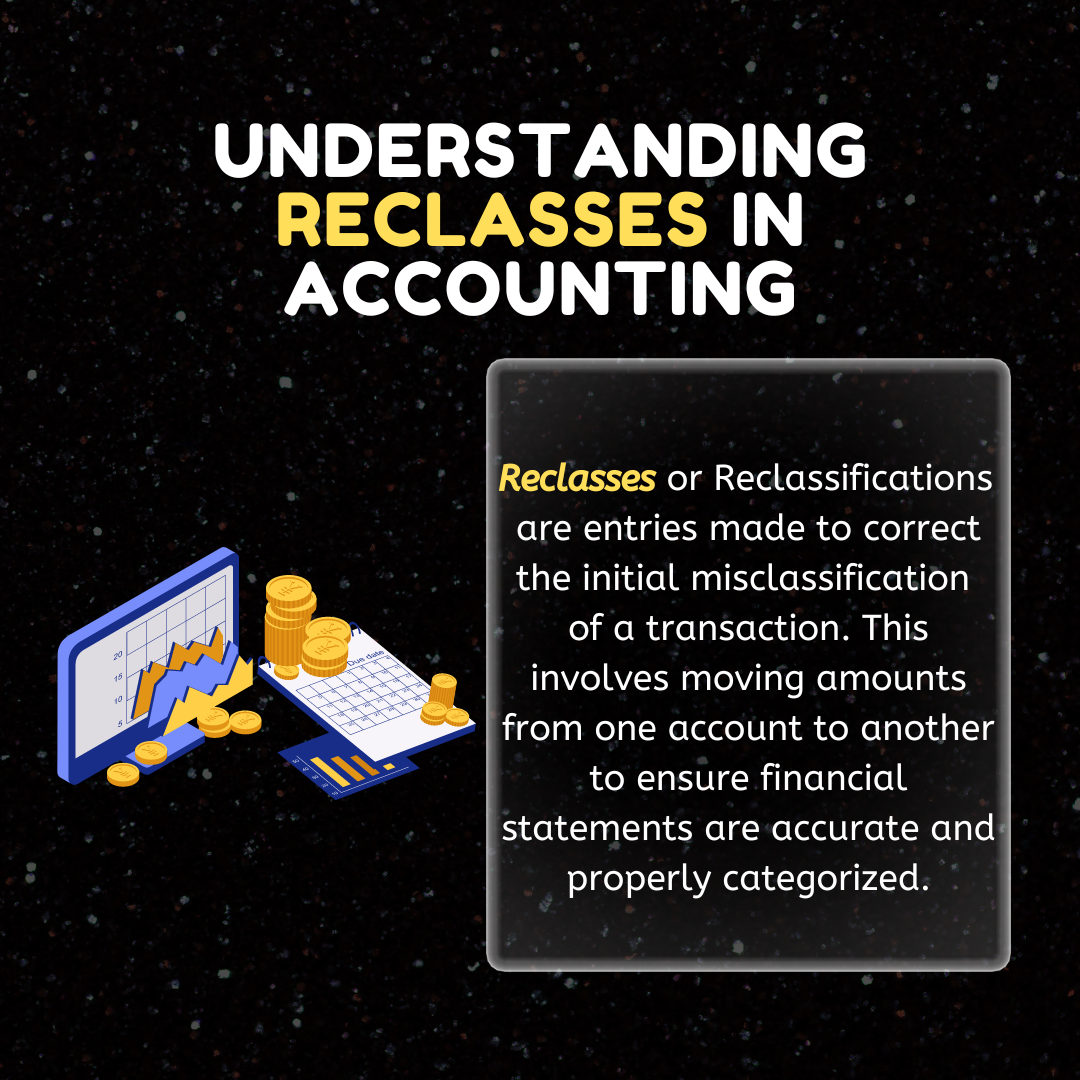

Exploring Reclasses in Accounting

Reclasses (reclassifications) are entries made to correct the classification of a transaction that was initially recorded incorrectly. This process involves moving amounts from one account to another to ensure that the financial statements are accurate and properly categorized.

Common Scenarios for Reclasses:

Misclassification of Expenses:

Correcting an expense that was initially recorded in the wrong category (e.g., moving office supplies from "Office Expenses" to "Supplies").

Reclassification of Revenues:

Adjusting revenue that was recorded in the wrong account (e.g., moving revenue from "Consulting Services" to "Product Sales").

Intercompany Transactions:

Correcting entries that involve transactions between different entities within the same organization.

Balance Sheet Adjustments:

Moving amounts between different asset, liability, or equity accounts to reflect accurate balances.

Importance of Reclasses:

Accuracy: Ensures that all transactions are correctly categorized, providing a clear and accurate financial picture.

Financial Analysis: Proper classification of transactions facilitates accurate financial analysis and reporting.

Internal Controls: Reclassifications are a part of maintaining strong internal controls and ensuring that financial data is reliable.

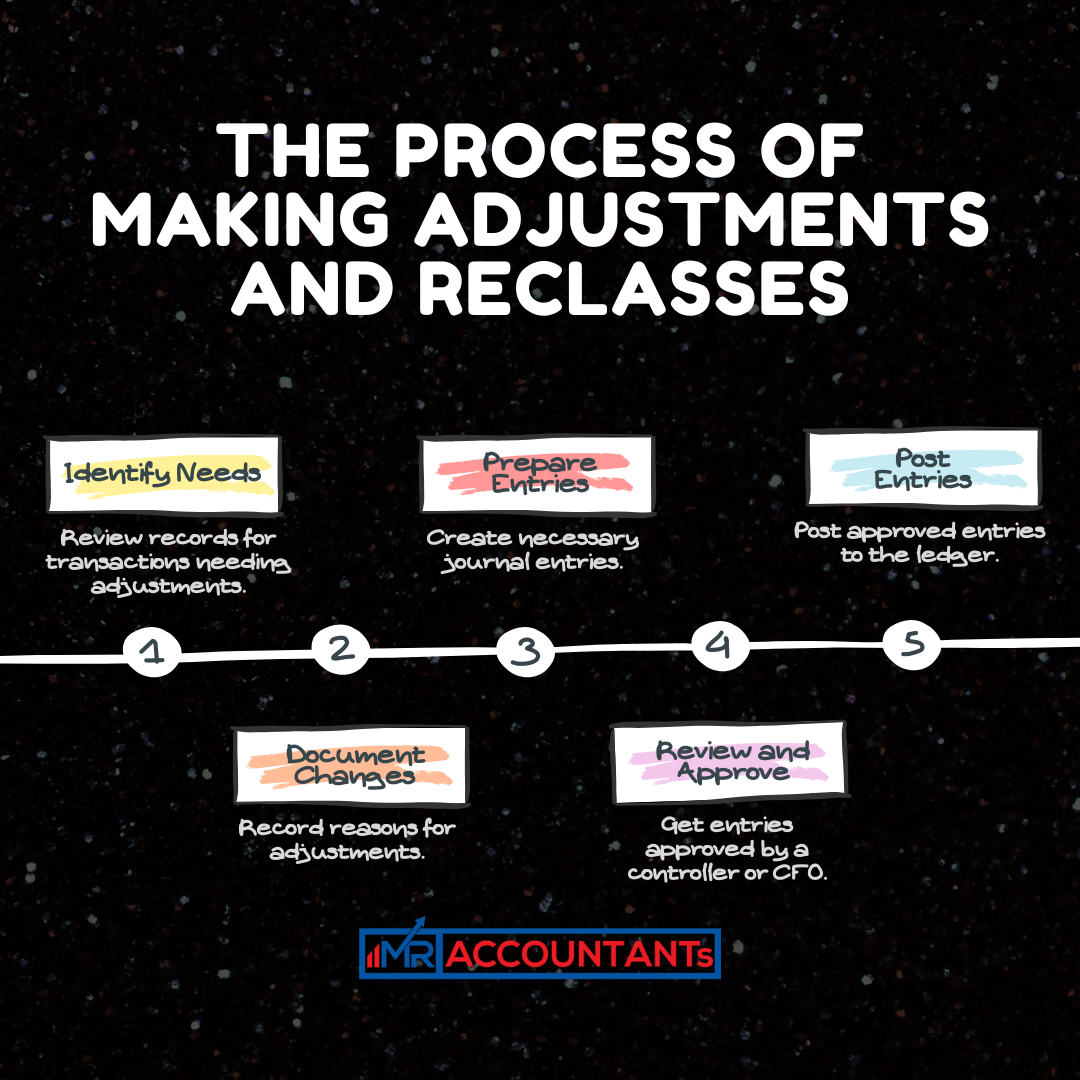

The Process of Making Adjustments and Reclasses

Identify the Need: Regularly review financial records to identify transactions that require adjustments or reclassification.

Document the Changes: Maintain detailed documentation of the reasons for the adjustments or reclassifications.

Prepare the Entries: Create journal entries to reflect the necessary adjustments or reclassifications.

Review and Approve: Have the entries reviewed and approved by a qualified individual, such as a controller or CFO.

Post the Entries: Once approved, post the entries to the general ledger.

Verify the Changes: After posting, review the financial statements to ensure that the adjustments or reclassifications were correctly applied.

Best Practices for Adjustments and Reclasses

Regular Review: Implement regular reviews of financial transactions to catch errors early.

Clear Policies: Establish clear policies and procedures for making adjustments and reclassifications.

Training: Ensure that accounting staff are well-trained in identifying and making necessary adjustments and reclassifications.

Use of Technology: Leverage accounting software to automate and streamline the process, reducing the risk of manual errors.

Conclusion

Adjustments and reclasses are vital components of the accounting process, ensuring the accuracy and integrity of financial statements. By understanding and implementing these processes effectively, organizations can maintain accurate financial records, comply with accounting standards, and make informed decisions. Regular reviews, clear policies, proper training, and the use of technology are key to mastering these essential accounting practices.