The Shape of Management Accounting to Come

In the dynamic landscape of business, where technology evolves rapidly and global markets fluctuate unpredictably, the role of management accounting is poised for a significant transformation. Traditionally seen as a function focused on financial reporting and cost control, management accounting is increasingly becoming a strategic partner in decision-making processes within organizations. As we look ahead, several key trends are shaping the future of this crucial discipline.

1. Integration of Technology: Advancements in technology, specifically artificial intelligence (AI), machine learning (ML), and data analytics, are ushering in a new era for management accounting. These technologies are not merely enhancing traditional practices but fundamentally transforming how management accountants operate within organizations.

Real-time Data Analysis:

One of the most significant impacts of AI and data analytics in management accounting is the ability to perform real-time data analysis. Traditional accounting methods often relied on historical data and periodic reports. Today, AI-powered algorithms can sift through vast amounts of data in real-time, identifying patterns and trends as they emerge. This capability enables management accountants to provide up-to-the-minute insights into financial performance, operational efficiencies, and market dynamics. For instance, AI can analyze sales trends across different demographics instantly, allowing managers to adjust pricing strategies promptly.

Predictive Modeling:

AI and ML algorithms excel in predictive modeling, leveraging historical data to forecast future outcomes with remarkable accuracy. In management accounting, predictive analytics can forecast cash flow, predict customer behavior, and anticipate market trends. By analyzing historical financial data alongside external factors such as economic indicators and industry trends, predictive models help management accountants make informed decisions about resource allocation, investment strategies, and risk management.

Scenario Planning:

Another powerful application of AI in management accounting is scenario planning. By creating multiple hypothetical scenarios based on different variables and assumptions, AI can simulate potential outcomes and their financial implications. This capability is invaluable for strategic decision-making, allowing organizations to assess the impact of various strategies and mitigate risks before implementation. For example, AI can simulate the effects of entering a new market, adjusting production capacity, or changing pricing structures, enabling management to choose the most optimal course of action.

Cloud Computing:

Cloud computing plays a pivotal role in enhancing the accessibility and collaboration capabilities of management accountants. Cloud-based accounting software allows real-time data sharing and collaboration among stakeholders across different locations. This accessibility enables management accountants to work seamlessly with other departments and external partners, facilitating faster decision-making processes. Moreover, cloud computing reduces the infrastructure costs associated with traditional IT setups and ensures data security through advanced encryption and backup protocols.

Strategic Decision Support:

Ultimately, the integration of AI, ML, data analytics, and cloud computing empowers management accountants to shift from a reactive to a proactive role within organizations. Instead of focusing solely on historical reporting and compliance, they become strategic advisors who leverage real-time insights and predictive capabilities to drive business growth and innovation. For example, by analyzing customer data in real-time, management accountants can recommend personalized marketing strategies that enhance customer engagement and loyalty.

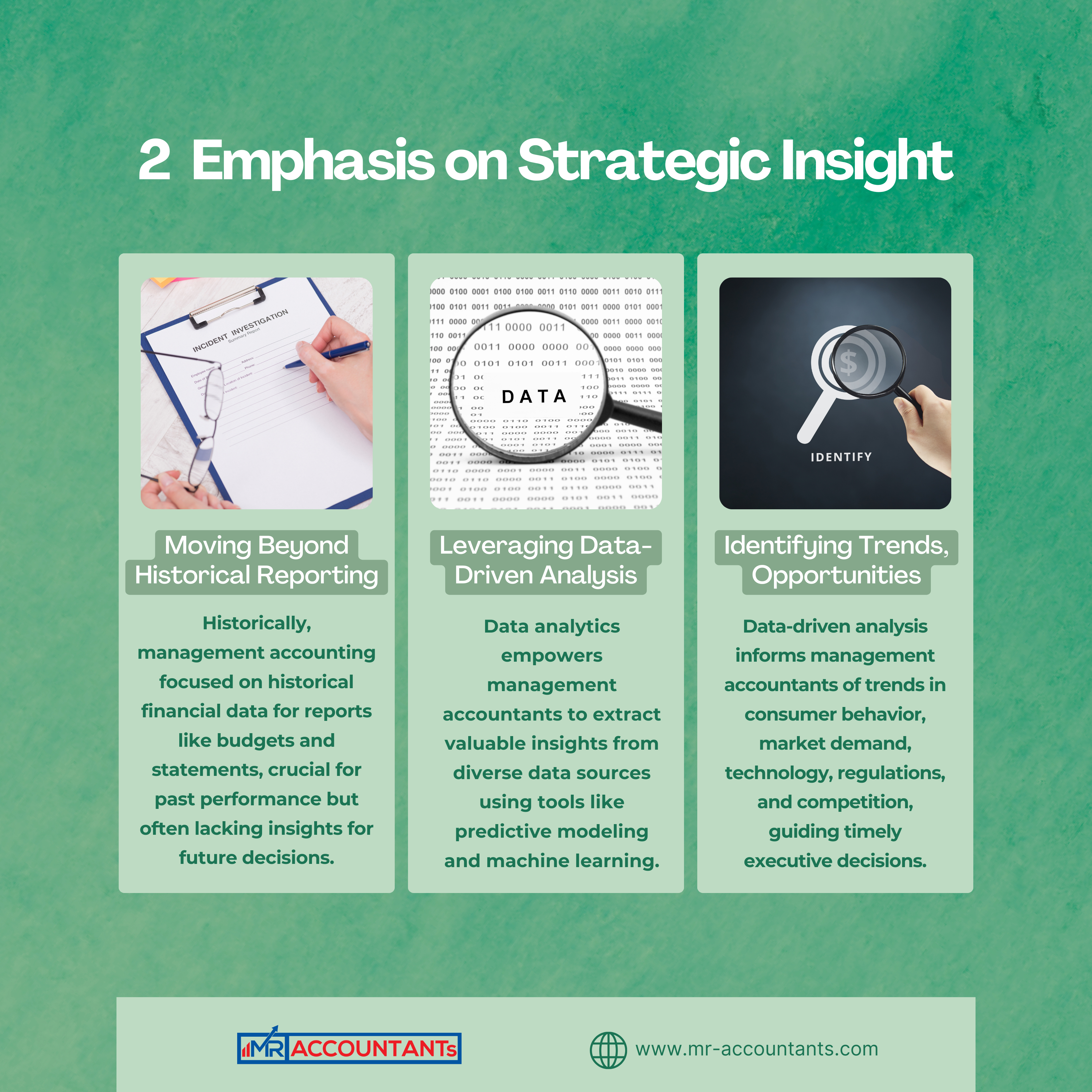

2. Emphasis on Strategic Insight: The shift towards emphasizing strategic insight marks a profound departure from traditional practices centered around retrospective financial reporting. This transformation is driven by the increasing availability of data and advancements in analytical tools, which enable management accountants to play a pivotal role in shaping the future direction of organizations.

Moving Beyond Historical Reporting:

Historically, management accounting primarily focused on compiling and analyzing historical financial data to produce reports such as budgets, variance analysis, and financial statements. While these reports are crucial for assessing past performance and compliance, they often fall short in providing actionable insights for future strategic decisions.

Leveraging Data-Driven Analysis:

With the advent of data analytics, management accountants now have access to a wealth of structured and unstructured data from various sources within and outside the organization. This includes financial data, operational metrics, customer feedback, market trends, and even social media sentiment. By harnessing sophisticated analytical tools and techniques such as predictive modeling, machine learning algorithms, and data visualization, management accountants can extract meaningful patterns and correlations from this data.

Identifying Trends, Opportunities, and Risks:

Data-driven analysis enables management accountants to identify emerging trends in consumer behavior, shifts in market demand, technological advancements, regulatory changes, and competitive threats. By uncovering these insights in real-time or near-real-time, they can provide timely recommendations to executive teams. For instance, predictive analytics can forecast future demand patterns based on historical sales data and external factors, helping businesses optimize inventory levels and production schedules proactively.

Enhancing Profitability and Sustainability:

The proactive approach of management accountants in providing strategic insights extends beyond profitability to encompass sustainability considerations. By analyzing environmental, social, and governance (ESG) metrics alongside financial performance, they can advise on integrating sustainability goals into business strategies. This might include assessing the financial implications of adopting renewable energy sources, optimizing supply chains to reduce carbon footprint, or investing in socially responsible initiatives that align with corporate values.

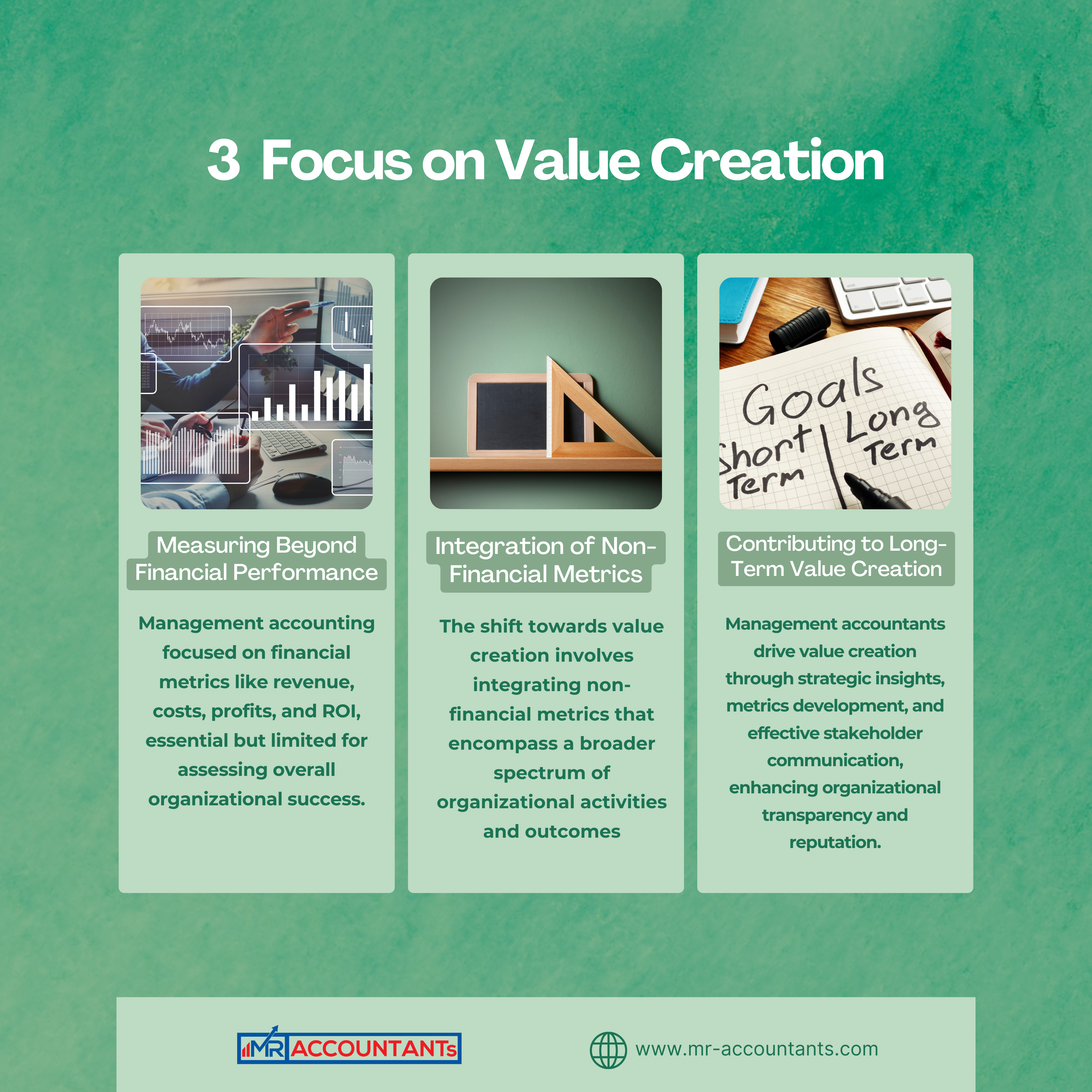

3. Focus on Value Creation: The traditional cost-centric approach of management accounting is evolving towards a focus on value creation. This shift involves measuring and communicating not only financial performance but also non-financial metrics such as customer satisfaction, innovation effectiveness, and environmental impact.

Integration of Non-Financial Metrics:

The shift towards value creation involves integrating non-financial metrics that encompass a broader spectrum of organizational activities and outcomes. These metrics may include:

Customer Satisfaction: Measuring customer satisfaction and loyalty indicators such as Net Promoter Score (NPS), customer retention rates, and feedback from customer surveys. Positive customer experiences not only drive repeat business but also contribute to brand reputation and market share growth.

Innovation Effectiveness: Assessing the organization's capability to innovate, develop new products or services, and improve existing offerings. Metrics may include the number of new product launches, success rates of innovation projects, and patents filed. Effective innovation enhances competitiveness and opens new revenue streams.

Environmental Impact: Evaluating the organization's environmental footprint, including greenhouse gas emissions, energy consumption, waste generation, and water usage. Sustainable practices not only contribute to regulatory compliance but also appeal to environmentally conscious consumers and investors.

Employee Engagement and Development: Monitoring metrics related to employee satisfaction, retention rates, training investments, and career development opportunities. Engaged and motivated employees are more productive, contribute to a positive organizational culture, and drive innovation and customer satisfaction.

Contributing to Long-Term Value Creation:

Management accountants play a crucial role in facilitating value creation by:

Providing Insights for Strategic Decision-Making: By analyzing both financial and non-financial data, management accountants offer insights that inform strategic decisions aimed at enhancing customer value, driving innovation, and improving sustainability.

Performance Measurement and Evaluation: Developing performance metrics that reflect the organization's strategic priorities and monitoring progress towards achieving them. This includes benchmarking against industry standards and best practices to identify areas for improvement.

Communicating Value to Stakeholders: Effectively communicating the organization's value creation initiatives and outcomes to stakeholders, including investors, customers, employees, and regulatory bodies. Transparent reporting builds trust and enhances the organization's reputation.

4. Cross-functional Collaboration: Cross-functional collaboration is becoming increasingly essential in modern management accounting practices as organizations recognize the interconnectedness of various departments and the need for integrated decision-making. This collaborative approach transcends traditional silos within organizations and fosters a more comprehensive understanding of business operations and strategic objectives.

Breaking Down Silos:

Historically, departments such as finance, marketing, operations, IT, and HR operated independently with limited interaction. This siloed approach could lead to fragmented decision-making and missed opportunities for synergy. However, as businesses evolve in response to dynamic market conditions and technological advancements, the need for collaboration across these functional areas has become paramount.

Holistic Understanding of Business Operations:

Cross-functional collaboration enables management accountants to gain a holistic understanding of how different parts of the organization contribute to overall performance. For example, by working closely with marketing teams, management accountants can analyze customer acquisition costs, evaluate marketing campaign ROI, and assess the effectiveness of promotional strategies. This collaboration ensures that financial strategies are aligned with marketing objectives and that resources are allocated optimally to maximize return on investment.

Integrated Decision-Making:

Effective management accounting requires integrating financial insights with operational realities and strategic goals. By collaborating with operations teams, management accountants can analyze production costs, optimize supply chain management, and identify opportunities for cost savings or efficiency improvements. This integrated approach ensures that financial decisions are grounded in operational feasibility and contribute directly to achieving organizational objectives.

Technology Facilitation:

Advancements in technology, particularly cloud-based collaboration tools and integrated enterprise resource planning (ERP) systems, facilitate cross-functional collaboration in management accounting. These tools enable real-time data sharing, collaborative budgeting and forecasting, and seamless communication across departments. For instance, cloud-based financial management systems allow finance and operations teams to access shared data and collaborate on budget revisions or resource allocation decisions in real-time.

Enhancing Strategic Alignment:

Cross-functional collaboration enhances strategic alignment across the organization. By engaging with IT teams, management accountants can leverage data analytics tools and IT infrastructure to enhance financial reporting capabilities, improve data accuracy, and strengthen cybersecurity measures. Collaboration with HR teams enables management accountants to analyze labor costs, assess workforce productivity, and develop strategies for talent management and retention that align with financial goals.

5. Ethical Considerations and Sustainability: As businesses face growing scrutiny regarding ethical practices and sustainability, management accountants play a pivotal role in ensuring transparency and accountability. They are instrumental in developing metrics to measure environmental, social, and governance (ESG) performance and in integrating sustainability goals into financial planning and reporting frameworks.

6. Skillset Evolution: The future management accountant requires a diverse skillset beyond technical proficiency. Skills in critical thinking, problem-solving, communication, and leadership are becoming increasingly important. Adaptability and a willingness to embrace continuous learning are essential as the profession evolves alongside technological advancements and changing business landscapes.

7. Regulatory and Reporting Changes: With regulatory requirements evolving globally, management accountants must stay informed and compliant while navigating complex reporting standards. This includes adapting to new regulatory frameworks and enhancing governance practices to mitigate risks and uphold organizational integrity.

Conclusion: The future of management accounting is one of transformation and opportunity. By embracing technological advancements, focusing on strategic insights, fostering collaboration, and integrating ethical considerations and sustainability, management accountants can elevate their role as strategic partners in driving organizational success. As businesses navigate an increasingly complex and interconnected world, the shape of management accounting to come promises to be innovative, adaptive, and indispensable.

In summary, management accounting is not merely evolving; it is undergoing a profound redefinition that positions it at the heart of strategic decision-making in modern organizations. As we embrace these changes, the profession stands ready to harness its full potential in shaping a sustainable and prosperous future for businesses worldwide.