The Importance of Bookkeeping for Small Business Success

In the fast-paced world of small business, keeping track of finances can often take a back seat to the daily demands of running the operation. However, one of the most critical factors for long-term success is solid bookkeeping. Effective bookkeeping is not just about recording numbers—it provides a foundation for financial stability, informed decision-making, and business growth. Let’s explore why bookkeeping is so vital for small businesses and how it can directly impact their success.

What is Bookkeeping?

Bookkeeping is the process of systematically recording, organizing, and managing a business’s financial transactions. This includes tracking income, expenses, assets, and liabilities. Bookkeepers ensure that all financial data is accurate, up-to-date, and compliant with legal regulations.

For small businesses, bookkeeping is typically handled using accounting software like QuickBooks, Xero, or FreshBooks, though some still rely on manual systems. Regardless of the method, the importance of proper bookkeeping cannot be overstated, as it affects every financial aspect of the business.

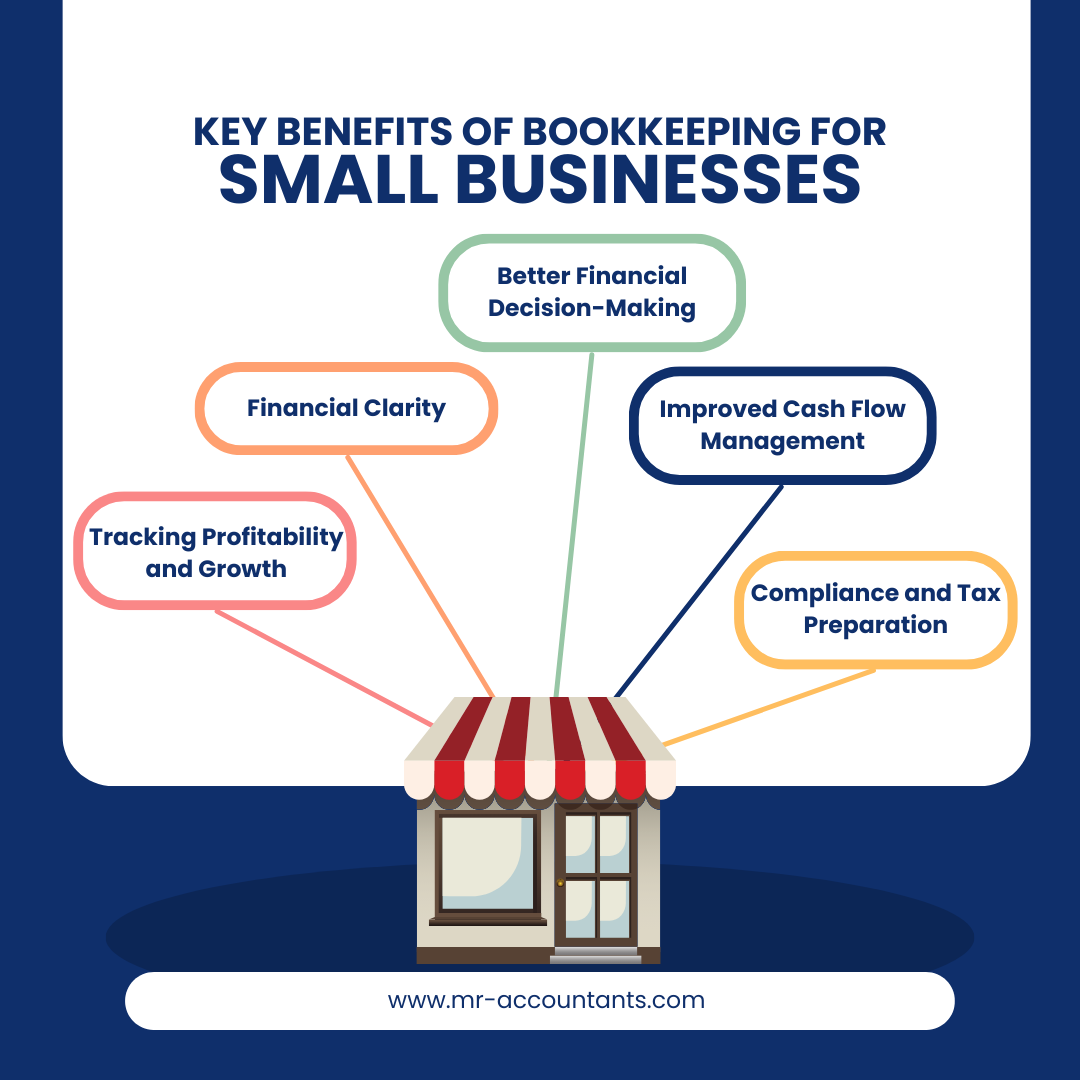

Key Benefits of Bookkeeping for Small Businesses

a. Financial Clarity

One of the primary advantages of bookkeeping is financial clarity. By recording every financial transaction, business owners can gain a clear understanding of their financial position. This includes knowing exactly how much cash is available, where expenses are going, and how much profit the business is making.

Without clear financial data, it becomes difficult to make informed decisions, and small businesses may quickly find themselves in financial trouble. Bookkeeping provides the foundation for this clarity.

b. Better Financial Decision-Making

Accurate bookkeeping allows business owners to make informed financial decisions. Whether you're considering expanding your business, launching a new product, or simply determining the right time to hire new staff, understanding your financial data is crucial.

With detailed records, you can spot trends, identify areas of waste, and allocate resources more efficiently. This ensures that decisions are not made based on guesswork but on real financial insights.

c. Improved Cash Flow Management

Cash flow is the lifeblood of any small business. Effective bookkeeping helps you monitor and manage cash flow by providing a detailed view of when money is coming in and going out. By staying on top of your cash flow, you can prevent shortfalls, avoid unnecessary debt, and ensure that you have enough cash to cover operational expenses.

Businesses with poor cash flow management often struggle to pay bills, suppliers, and even employees. Bookkeeping ensures that these problems are avoided by giving business owners a clear picture of their cash flow situation at all times.

d. Compliance and Tax Preparation

Small businesses are required to comply with various local, state, and federal tax regulations. Accurate bookkeeping makes tax preparation much simpler by ensuring that all income and expenses are properly recorded. Come tax season, you won’t have to scramble to find receipts or worry about missed deductions.

Moreover, good bookkeeping helps you avoid legal issues. By keeping accurate and up-to-date financial records, you ensure that your business complies with tax regulations, reducing the risk of audits, penalties, or fines.

e. Tracking Profitability and Growth

Bookkeeping isn’t just about balancing the books; it’s also an essential tool for tracking your business’s profitability and growth. By keeping an eye on your income and expenses over time, you can gauge how profitable your business is and identify growth opportunities.

Detailed financial records allow you to set realistic goals, track your progress, and adjust your business strategy based on actual performance data. Without proper bookkeeping, it’s nearly impossible to understand whether your business is thriving or heading toward trouble.

f. Access to Funding and Investment Opportunities

When seeking loans or investments, financial transparency is key. Lenders and investors want to see clear and accurate financial records before they commit to providing capital. A well-maintained set of books can demonstrate that your business is financially sound and capable of managing new funds responsibly.

Conversely, poor bookkeeping can be a red flag to potential investors or lenders, signaling that your business may be disorganized or risky.

g. Stress Reduction for Business Owners

Running a small business is stressful enough without the added worry of messy financial records. By keeping your books in order, you can reduce stress and focus on what matters most—growing your business. When you know that your financial data is accurate and up to date, you can confidently make decisions without second-guessing yourself.

Common Bookkeeping Mistakes Small Businesses Should Avoid

While the benefits of bookkeeping are clear, small businesses often make mistakes that can undermine its effectiveness. Here are a few common pitfalls to avoid:

a. Mixing Personal and Business Finances

One of the most common mistakes is failing to separate personal and business finances. This can lead to confusion, inaccurate records, and potential legal issues. It’s important to maintain separate accounts and keep your business expenses separate from personal ones.

b. Neglecting to Keep Records Updated

Falling behind on bookkeeping is another major issue. Waiting too long to record transactions can lead to mistakes, missing information, and poor financial visibility. Make it a habit to update your books regularly, whether weekly or monthly, to avoid last-minute stress.

c. Not Backing Up Financial Data

In today’s digital world, losing financial data due to a computer crash or software error can be devastating. Always ensure that your financial records are backed up, either through cloud storage or an external drive, to protect your business from data loss.

How to Set Up Effective Bookkeeping for Your Small Business

Setting up a solid bookkeeping system for your small business doesn’t have to be difficult. Here’s a quick guide to get you started:

Choose the Right Software: Select accounting software that meets your business’s needs. Popular options include QuickBooks, Xero, and FreshBooks.

Open a Business Bank Account: Keep personal and business finances separate by opening a dedicated business bank account.

Track Income and Expenses: Make it a habit to track every transaction, from sales and revenue to expenses like rent, supplies, and wages.

Reconcile Accounts Regularly: Reconcile your bank accounts regularly to ensure that your records match your actual financial transactions.

Hire a Bookkeeper or Outsource: If managing your books becomes too overwhelming, consider hiring a bookkeeper or outsourcing to a professional bookkeeping service.

Conclusion

Bookkeeping is not just an administrative task—it’s a critical component of small business success. By maintaining accurate and up-to-date financial records, businesses can make informed decisions, improve cash flow, ensure compliance, and track growth. Whether you manage your books in-house or outsource to a professional, prioritizing bookkeeping will set your small business up for long-term success.

If you’re struggling with bookkeeping, now is the time to invest in a system that works for you. Your business’s financial health—and future success—depend on it.