Understanding Accounting Standards: Enhancing Financial Transparency

Accounting standards serve as the backbone of financial reporting, fostering transparency and comparability across industries and countries. In this article, we'll delve into the significance of accounting standards, focusing on the two primary frameworks: Generally Accepted Accounting Principles (GAAP) in the United States and International Financial Reporting Standards (IFRS) adopted globally.

Understanding Accounting Standards

At its essence, accounting standards are a set of guidelines and rules established by regulatory bodies or professional organizations. These standards dictate how financial transactions should be recorded, reported, and disclosed in financial statements. They provide a common language for businesses, investors, regulators, and other stakeholders to understand and evaluate financial performance accurately.

Accounting standards promote transparency by ensuring that financial information is reported in a consistent and comparable manner. This transparency is essential for investors, creditors, and other stakeholders to assess the financial health and performance of a company accurately. By adhering to standardized accounting principles, companies enable stakeholders to make informed decisions. Whether it's assessing investment opportunities, evaluating creditworthiness, or analyzing performance trends, consistent financial reporting fosters confidence and clarity in decision-making processes. Regulatory bodies and stock exchanges often mandate the use of specific accounting standards to ensure compliance and maintain market integrity. Adherence to these standards is not only a legal requirement but also a testament to a company's commitment to ethical and transparent business practices.

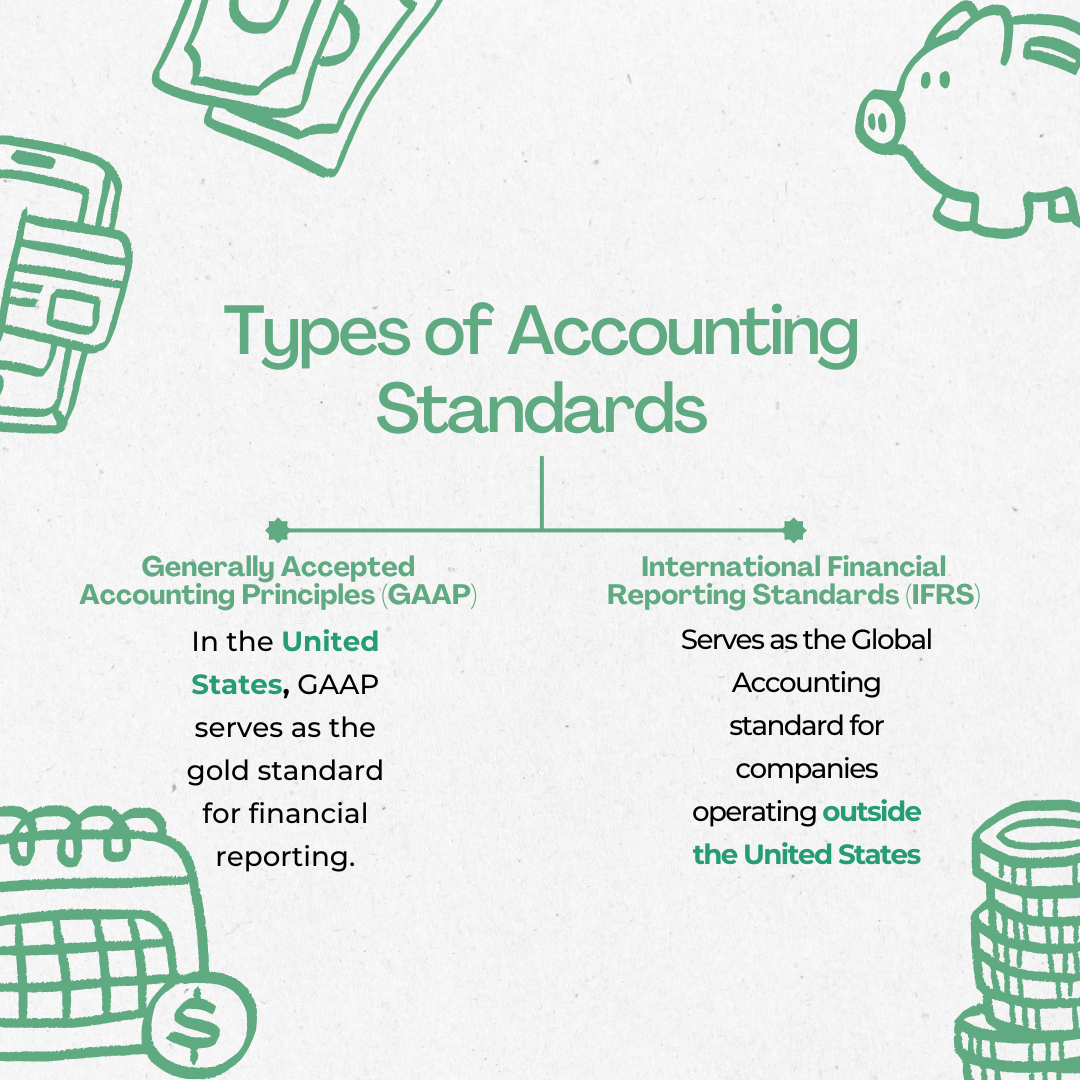

Types of Accounting Standards

Generally Accepted Accounting Principles (GAAP)

International Financial Reporting Standards (IFRS)

Generally Accepted Accounting Principles (GAAP)

In the United States, GAAP serves as the gold standard for financial reporting. Developed and managed by the Financial Accounting Standards Board (FASB), GAAP provides a comprehensive framework for public and private companies, as well as nonprofit organizations, to prepare their financial statements. Adherence to GAAP is mandatory for listed companies on U.S. securities exchanges, as required by the Securities and Exchange Commission (SEC).

Clarity and Consistency:

Enhanced Communication: GAAP aims to improve the clarity of financial information communicated to stakeholders. By adhering to standardized accounting principles, companies ensure that their financial statements are easily understandable and interpretable by investors, creditors, and other users.

Consistency Across Entities: Consistency is crucial for comparability. GAAP provides a consistent framework for financial reporting, allowing stakeholders to compare the financial performance and position of different entities accurately. This consistency enhances trust and facilitates decision-making processes.

Reduction of Misinterpretation: Clear and consistent financial reporting reduces the risk of misinterpretation or misunderstanding of financial information. It helps mitigate the potential for errors or discrepancies in financial analysis and decision-making.

Financial Statement Presentation:

Structured Reporting: GAAP provides guidelines on how financial statements should be structured, ensuring uniformity and coherence in presentation. This includes the format, order of items, classifications, and the use of headings, subtotals, and notes to the financial statements.

Disclosure Requirements: GAAP mandates the disclosure of significant information in financial statements to provide users with a comprehensive understanding of an entity's financial position, performance, and cash flows. These disclosures include accounting policies, assumptions, estimates, and significant events or transactions.

Transparency and Accountability: The structured presentation of financial statements under GAAP enhances transparency and accountability. Stakeholders can easily access and analyze relevant information, enabling them to hold management accountable for the entity's financial performance and decisions.

Recognition and Measurement:

Accurate Representation: GAAP specifies criteria for recognizing and measuring various financial elements such as revenue, assets, liabilities, and expenses. This ensures that financial information accurately reflects the economic reality of transactions and events, providing a true and fair view of the entity's financial position and performance.

Conservative Principles: GAAP incorporates conservative principles to mitigate the risk of overstating assets or income and understating liabilities or expenses. This conservative approach promotes prudence and reliability in financial reporting, reducing the likelihood of financial misstatements or manipulation.

Comparability and Reliability: By establishing consistent criteria for recognition and measurement, GAAP enhances comparability and reliability in financial reporting. Stakeholders can rely on the consistency and accuracy of financial information to make informed decisions and assess the entity's financial health and performance accurately.

International Financial Reporting Standards (IFRS)

IFRS, developed by the International Accounting Standards Board (IASB), serves as the global accounting standard for companies operating outside the United States. It aims to harmonize accounting practices worldwide, promoting consistency and comparability in financial reporting. While IFRS and GAAP share many similarities, there are notable differences in certain accounting treatments and principles.

Global Consistency:

Uniform Reporting Standards: IFRS provides a common framework for financial reporting, ensuring consistency in the preparation and presentation of financial statements across countries and industries. This consistency facilitates cross-border investment and analysis by investors, creditors, and other stakeholders.

Harmonization of Practices: IFRS aims to harmonize accounting practices worldwide, reducing disparities and complexities associated with multiple sets of accounting standards. This harmonization streamlines financial reporting processes for multinational companies and promotes a level playing field in the global marketplace.

Enhanced Comparability: By adopting IFRS, companies can improve the comparability of their financial statements with those of other entities operating in different jurisdictions. This comparability enables stakeholders to assess performance, risks, and opportunities more effectively, contributing to better-informed decision-making.

Flexibility and Adaptability:

Responsive to Change: IFRS is designed to be flexible and adaptable to evolving business practices, economic conditions, and regulatory requirements. The International Accounting Standards Board (IASB) regularly reviews and updates IFRS to address emerging issues and ensure its relevance in a dynamic global environment.

Tailored Application: IFRS allows for variations in application based on the specific circumstances and complexities of individual transactions or industries. This flexibility enables companies to apply accounting principles that best reflect the economic substance of their transactions while complying with the overarching principles of IFRS.

Facilitation of Innovation: The adaptability of IFRS encourages innovation and creativity in financial reporting practices. Companies can explore new business models and structures without being constrained by rigid accounting rules, fostering a culture of continuous improvement and value creation.

Principle-Based Approach:

Emphasis on Substance Over Form: IFRS adopts a principle-based approach, focusing on the economic substance of transactions rather than their legal form. This approach allows for more judgment and interpretation in financial reporting, enabling companies to reflect the underlying economics of their business activities accurately.

Promotion of Professional Judgment: Unlike the rules-based nature of Generally Accepted Accounting Principles (GAAP), which may lead to compliance-driven behavior, IFRS encourages professional judgment and critical thinking among preparers and auditors. This promotes a deeper understanding of the business and its financial implications.

Adaptability to Diverse Situations: The principle-based nature of IFRS allows for greater adaptability to diverse business situations and transactions. It accommodates a wide range of industries, business models, and regulatory environments, enabling companies to apply accounting standards that best reflect their unique circumstances.

Accounting standards play a pivotal role in promoting transparency, credibility, and comparability in financial reporting. Whether it's GAAP in the United States or IFRS adopted globally, adherence to these standards ensures that stakeholders have access to relevant, accurate, and reliable financial information. As businesses operate in an increasingly interconnected world, the importance of accounting standards in facilitating trust and informed decision-making cannot be overstated. By following these standards, organizations contribute to a more robust and sustainable global financial ecosystem.