What is Bookkeeping?

At its core, bookkeeping involves the systematic recording, organizing, and tracking of financial transactions within a business. It encompasses tasks such as recording income and expenses, reconciling accounts, and generating financial reports. While it may not be the most glamorous aspect of running a business, it serves as the foundation for sound financial management.

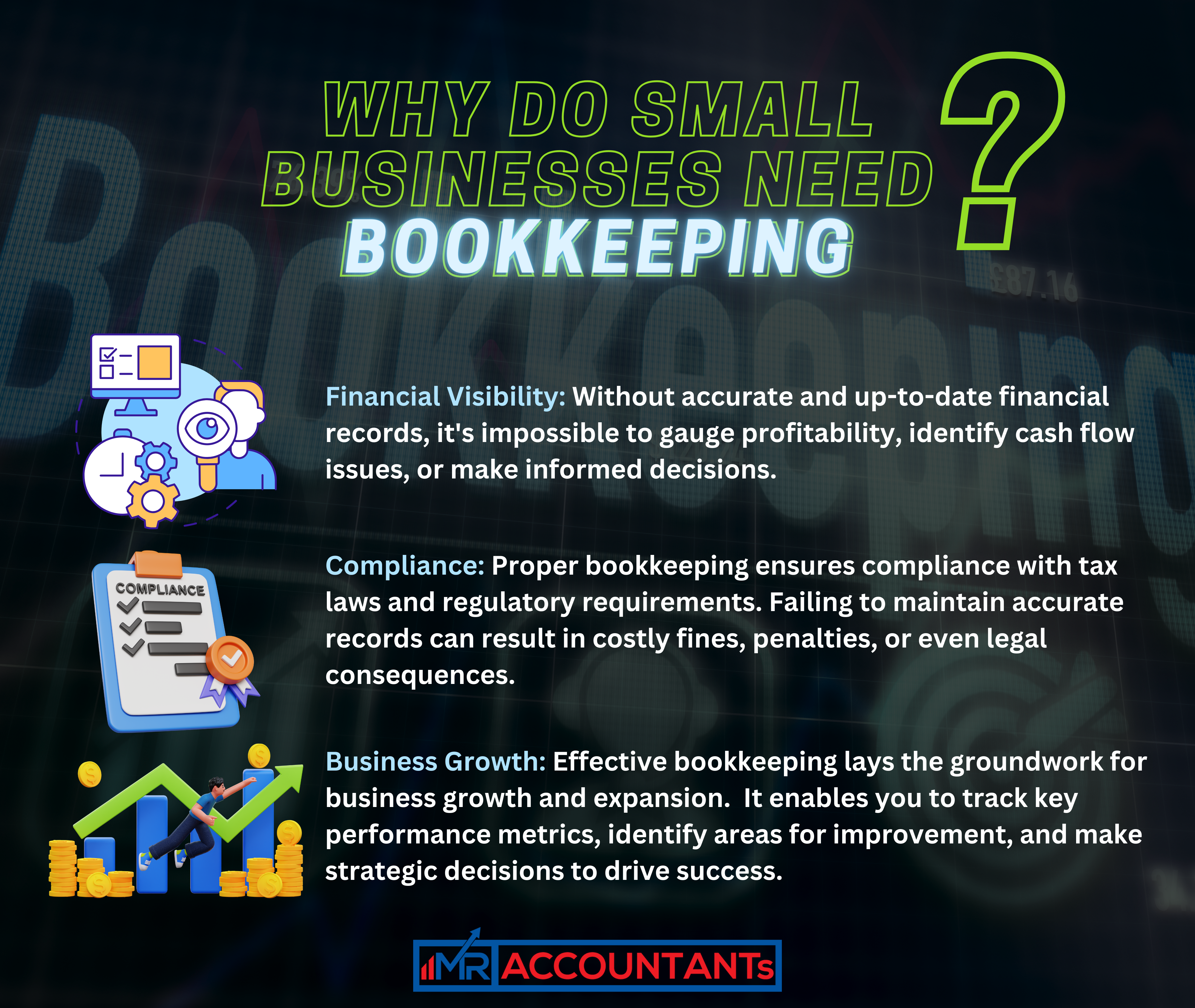

Why Do Small Businesses Need Bookkeeping?

Financial Visibility: Bookkeeping provides small business owners with a clear understanding of their financial health. Without accurate and up-to-date financial records, it's impossible to gauge profitability, identify cash flow issues, or make informed decisions.

Compliance: Proper bookkeeping ensures compliance with tax laws and regulatory requirements. Failing to maintain accurate records can result in costly fines, penalties, or even legal consequences.

Business Growth: Effective bookkeeping lays the groundwork for business growth and expansion. It enables you to track key performance metrics, identify areas for improvement, and make strategic decisions to drive success.

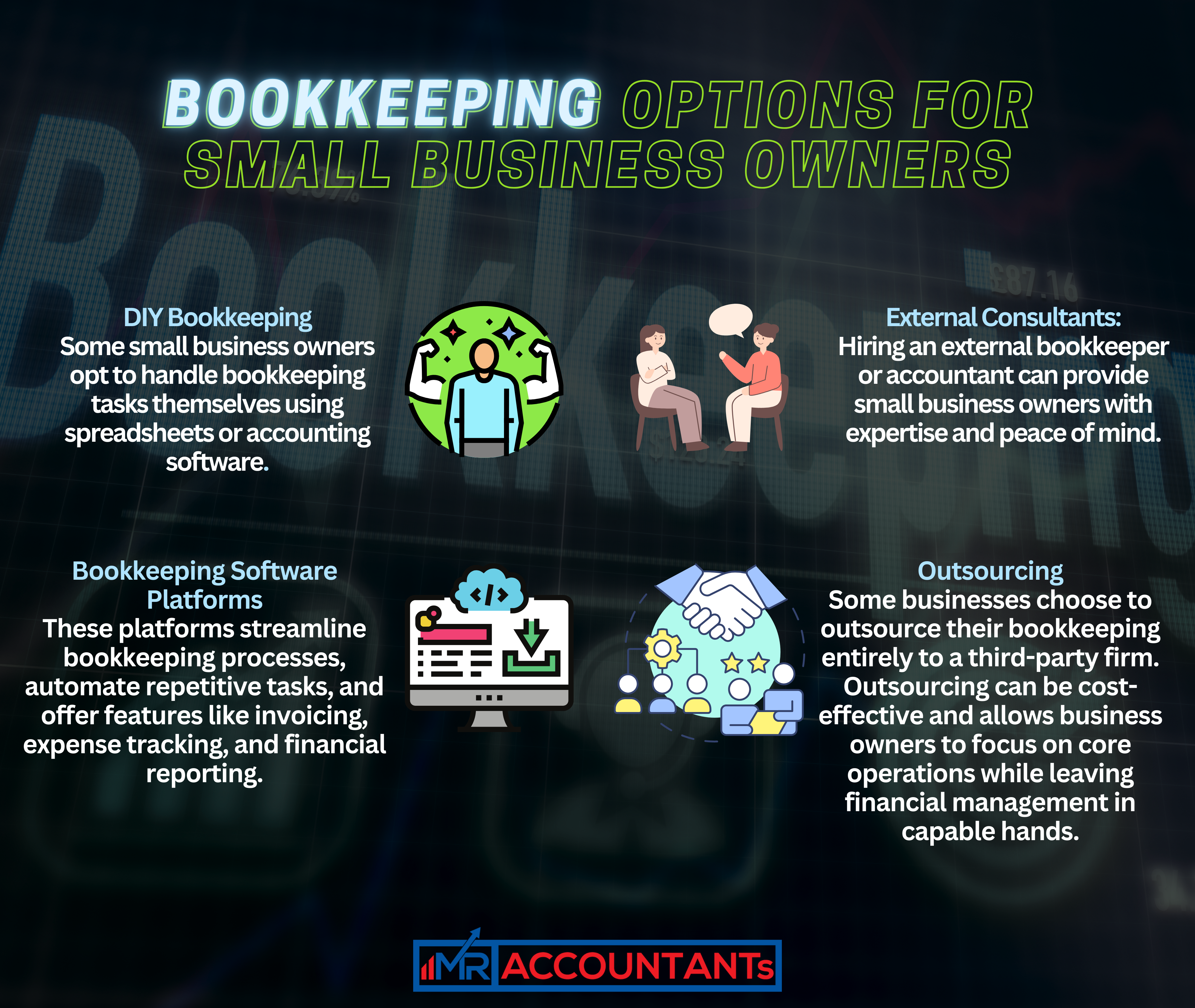

Bookkeeping Options for Small Business Owners:

DIY Bookkeeping: Some small business owners opt to handle bookkeeping tasks themselves using spreadsheets or accounting software. While this approach can save money, it requires a significant time investment and may lack the expertise needed for complex financial management.

Bookkeeping Software Platforms: There's a myriad of bookkeeping software options available, such as QuickBooks, Xero, and FreshBooks. These platforms streamline bookkeeping processes, automate repetitive tasks, and offer features like invoicing, expense tracking, and financial reporting.

External Consultants: Hiring an external bookkeeper or accountant can provide small business owners with expertise and peace of mind. These professionals can handle all aspects of bookkeeping, from day-to-day transactions to tax preparation and financial analysis.

Outsourcing: Alternatively, some businesses choose to outsource their bookkeeping entirely to a third-party firm. Outsourcing can be cost-effective and allows business owners to focus on core operations while leaving financial management in capable hands.

The Pitfalls of Neglecting Bookkeeping:

Financial Mismanagement: Without proper bookkeeping, small businesses risk mismanaging their finances, leading to cash flow problems, overdrawn accounts, and missed opportunities.

Tax Troubles: Inaccurate or incomplete financial records can result in errors on tax returns, triggering audits or investigations by tax authorities.

Poor Decision-Making: Without access to timely and accurate financial information, small business owners may make ill-informed decisions that jeopardize their long-term success.

Legal Liabilities: Failure to comply with tax laws or regulatory requirements can expose small businesses to legal liabilities, tarnishing their reputation and undermining trust with customers and stakeholders.

Step-by-Step Process:

Bookkeeping may seem like a daunting task for small business owners, especially for those who lack prior experience or financial expertise. However, establishing sound bookkeeping practices is essential for maintaining financial health and facilitating business growth. In this guide, we'll walk you through the steps to start bookkeeping in your small business, from setting up your system to managing day-to-day transactions and staying compliant with tax regulations.

Step 1: Understand the Basics

Before diving into bookkeeping, it's crucial to familiarize yourself with the fundamentals. Learn the difference between bookkeeping and accounting, understand basic accounting principles like double-entry bookkeeping, and acquaint yourself with financial statements such as the balance sheet, income statement, and cash flow statement.

Step 2: Choose Your Method

Decide on a bookkeeping method that suits your business needs and preferences. While some businesses opt for manual methods using spreadsheets or paper ledgers, many prefer to use accounting software for its efficiency and accuracy. Research and select a reputable accounting software platform that aligns with your budget and requirements.

Step 3: Set Up Your Chart of Accounts

Create a chart of accounts tailored to your business structure and industry. A chart of accounts is a categorized list of all the accounts used by your business to record financial transactions. Common categories include assets, liabilities, equity, revenue, and expenses. Customize your chart of accounts to accurately reflect your business's operations and financial activities.

Step 4: Record Transactions

Start recording transactions as they occur. This includes sales, purchases, expenses, and any other financial activities relevant to your business. Be diligent about categorizing transactions correctly to ensure accurate financial reporting. Depending on your chosen method, you may manually enter transactions into your accounting software or upload bank statements for automated reconciliation.

Step 5: Reconcile Accounts

Regularly reconcile your bank accounts, credit cards, and other financial accounts with your accounting records. Reconciliation ensures that your records match your actual financial transactions, helping to identify discrepancies and errors. Perform reconciliations on a monthly basis to maintain accuracy and integrity in your financial data.

Step 6: Generate Financial Reports

Use your accounting software to generate financial reports such as balance sheets, income statements, and cash flow statements. These reports provide valuable insights into your business's financial performance, liquidity, and profitability. Review financial reports regularly to monitor trends, identify areas for improvement, and make informed business decisions.

Step 7: Stay Compliant

Stay up-to-date with tax laws and regulations applicable to your business. Keep accurate records of income, expenses, and deductions to facilitate tax filing and compliance. Consider consulting with a tax professional or accountant to ensure that you meet all tax obligations and take advantage of available tax-saving opportunities.

How To Do Bookkeeping For a Small Business

Setting up an ongoing bookkeeping system for your small business is essential for maintaining financial stability and ensuring smooth operations. Here's a detailed breakdown of the basic bookkeeping principles to establish a reliable bookkeeping process:

Keep Your Receipts:

Detailed Records: Maintain detailed records of all transactions, including sales and purchases. Record the amount, date, and any other pertinent information.

Proof of Transactions: Retain purchase receipts as proof of transactions. This documentation is crucial for verifying expenses and justifying deductions during tax filing.

Keep a Ledger:

Digital Ledger: Utilize a digital ledger or accounting software to record and track financial transactions. This serves as a central repository for summarizing your business's financial performance.

Categories: Categorize transactions into revenues, business expenses, and any other financial information relevant to your business operations.

Create Financial Reports:

Profit and Loss: Prepare a profit and loss statement to analyze your business's revenue, expenses, and net income over a specific period.

Balance Sheet: Generate a balance sheet to assess your business's assets, liabilities, and equity at a given point in time.

Cash Flow Analysis: Conduct a cash flow analysis to monitor the inflow and outflow of cash and identify potential cash flow issues.

Aged Accounts Receivables and Payables: Monitor aged accounts receivables to track outstanding customer payments and aged accounts payables to manage pending vendor payments effectively.

Proactively Handle Tax Liabilities

Detailed Records: Maintain organized records of business transactions throughout the year to streamline the tax filing process.

Collaboration with Professionals: Work closely with your CPA or tax filing expert, providing them with accurate financial statements for tax preparation.

Cloud-Based Accounting Software: Consider utilizing cloud-based accounting software like FreshBooks to automate bookkeeping tasks and facilitate collaboration with accountants and bookkeepers. These platforms offer features tailored to small businesses and can simplify tax compliance processes.

6 Tips for Small Business Bookkeeping

Here are six essential tips for small business bookkeeping to help beginners get started quickly and efficiently:

Bring Your Bookkeeper Up to Speed:

Collect Relevant Records: Gather all past records, transactions, and financial statements to provide your bookkeeper with a comprehensive overview of your business's financial history.

Establish Financial Context: Ensure your bookkeeper has access to all relevant information needed to accurately track and manage your finances from the outset.

Keep Personal and Business Costs Separate:

Separate Bank Accounts: Maintain separate bank accounts for personal and business finances to avoid confusion and streamline bookkeeping processes.

Clear Distinction: Avoid commingling personal and business transactions, as this can complicate financial reporting and tax filing.

Track Absolutely Everything:

Accurate Expense Tracking: Monitor all business transactions diligently, including expenses, receipts, and

Proactive Tax Planning: Anticipate upcoming financial obligations, including taxes and payroll taxes, and plan accordingly to ensure timely payments.

Documentation

Establish Emergency Fund: Work with your bookkeeper and accountant to determine an appropriate emergency fund to cover unexpected expenses.

Cash Flow Forecasting: Utilize cash flow forecasting to assess liquidity needs and ensure adequate cash reserves are maintained without compromising investment opportunities.

Regularly Cross-Check and Audit Files:

Implement Reconciliation Practices: Incorporate regular reconciliations of financial records with source documents such as bank statements, receipts, and invoices.

Promote Transparency and Compliance: Regular cross-checking and auditing of files enhance communication, transparency, and compliance with accounting standards and regulations.